Related: How to reduce your building insurance premium

We must state that every building is different and that it is important to discuss the requirements of each policy with a qualified person. There are however typical ‘risks’ that a landlords building insurance policy will cover. Typically, these risks are:

Almost as important when considering the risks covered are the risks that are NOT covered. These risks can cause confusion with questions such as ‘does building insurance cover damp’ only causing delays in resolving the matter. Typical risks not covered are:

Now that we have covered what risks are covered in building insurance for flats, let’s take a look at how you get a policy.

Strangford Management use the services of an independent insurance brokerage (St. Giles Insurance & Finance Services Limited if you want to know more). You too have the ability to use a brokerage or simply direct your quotation request to an insurer of your choice. In both cases they will need to know certain, important, bits of information before they can give you an accurate quotation:

After this information has been provided, you should be in a position to obtain the most accurate quotation for your building.

As we mentioned previously, Strangford Management use an insurance brokerage to obtain the most competitive landlords building insurance policy for our clients under our block management London portfolio. Whilst our clients are in a position to instruct us to use a specific insurance company, below are our top 3 reasons why we would suggest using a broker:

1 – Access: Insurance brokerages have established relationships with insurance companies meaning that you have not only access to 1 quotation but an entire market. Great news when you have to justify the service charge spend!

2- Ease: following on from the above point, we all understand that being a Director of a Residents Management Company is a part time, voluntary role and therefore efficiency is key. The last thing you want is to be making hours of phone calls and emails to sort out an insurance policy. So long as you have the information we have mentioned above then you can let the brokerage do all the running.

3 – Cost: contrary to popular belief, insurance brokers do have access to specialist underwriters and therefore they can actually obtain quotations for you that you may otherwise not have access to, and we all like value for money don’t we!

So we have informed you what your landlords building insurance policy covers, how to get the best insurance policy and the reasons to use an insurance brokerage. Now we want to inform you of how to make a claim once you have your policy in place.

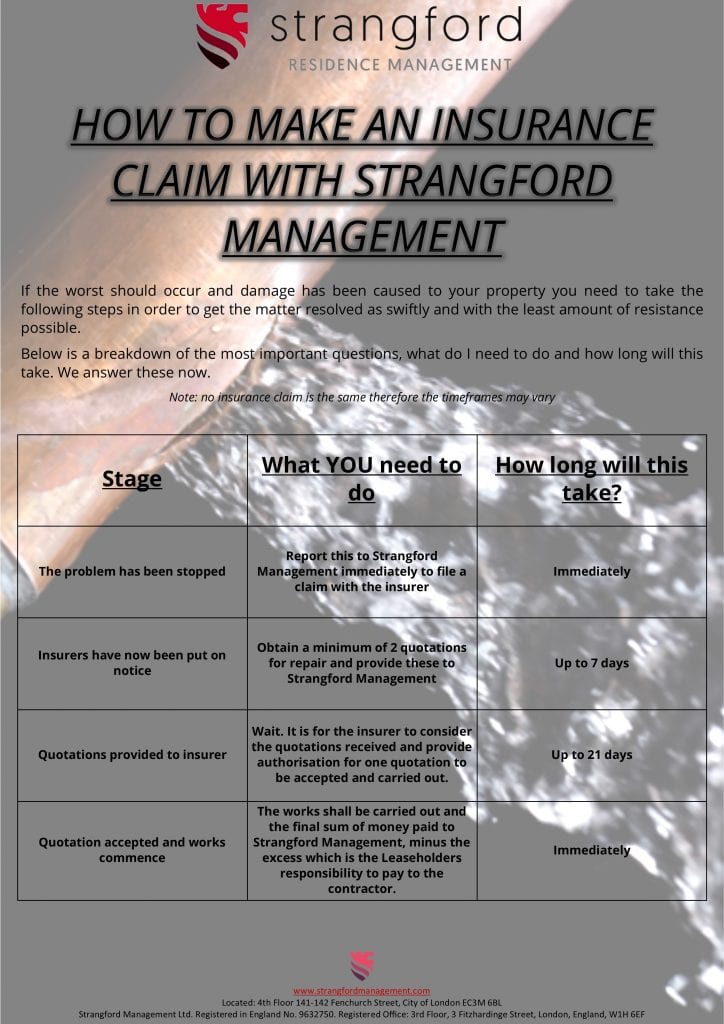

We understand, you may have just had a water leak into your flat, its damaged your oak wooden flooring, ruined your Farrow & Ball painted walls and damaged the Victorian cornices! So the very last thing you need to be obstructed with is an overly complicated claiming process. As such, we have created the below colourful graphic to show just how quick and simple it is to make your claim:

So now we have told you everything you need to know about landlord building insurance, the next step is for you to contact Strangford Management, providing leading block management London, we can help reduce the cost of your building insurance premiums today.

Initially designed for buildings over 18 metres tall, the EWS1 form requirements now affect…

NHBC Buildmark Cover holds 80-90% market share in the new home warranty market. Understanding…

Britain's cladding crisis affects nearly half a million people nationwide. Only one-third of dangerous…

Service charge disputes are the biggest problem between leaseholders and landlords in the UK…

The government will reshape the scene of property ownership in England and Wales through…

Wooden flooring, ranging from laminate options to authentic hardwood, has become a sought-after choice for…

{kind=link}

View Comments

I don't think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Your article helped me a lot, is there any more related content? Thanks!

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.